Open Market Shared Equity (OMSE) is a Scottish Government incentive to help first-time buyers purchase a property on the open market where it is affordable for them to do so.

In January, it was announced that OMSE would receive another £80m of funding for the financial year 2016/17.

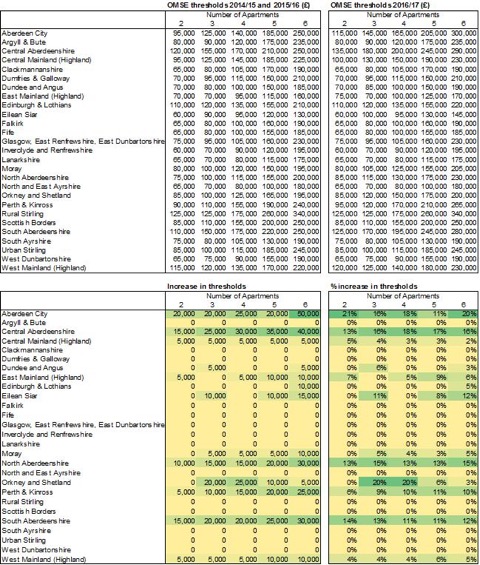

There are maximum price limits (known as threshold limits) by area to ensure only starters homes are bought under the scheme. Most threshold limits cover a local authority area; the Scottish Government agreed that areas would be set as wide as possible to allow potential purchases to search for a property over a wider area.

So how exactly does OMSE work?

Example (from gov.scot)

If you are eligible to purchase a home up to a maximum price of £100,000 and you can afford to contribute £70,000 (the maximum mortgage that you can raise plus any personal contribution) you would hold a 70 per cent stake in your home and the Scottish Government would provide assistance of the remaining £30,000.

When you apply to buy a house, you will have to state all your sources of finance. Your funds will be considered to be the total of:

- gross earnings, per single person or couple, as appropriate;

- any other income, comprising sickness benefit, unemployment benefit, bank interest, superannuation or pension from previous employment, working families tax credit, widow’s pension and shareholder’s profits; and

- personal contributions.

Personal contributions may include, for example, savings and gifts. The definition of savings that we use includes: cash; premium bonds; stocks and shares; unit trusts; bank or building society accounts and fixed-term investments; the surrender value of any endowment policies; property; redundancy payments; and pension lump sum payments.

You may keep £5,000 of any personal contribution you can make – this will help you to fund the costs of buying your home (such as your legal costs, registration fees, mortgage arrangement fees and any removal costs). Above this amount, 90 per cent of the balance will need to be treated as a deposit contribution towards the cost of your home.